Red Card of Macro Risks

The demographic slowdown in China will be felt from 2020 onwards, leading to a scenario similar to Japan after 1990. The very high debt levels in China (300% of GDP) are an indication of high levels of over investment. Demographic demand slowed from 2020 and is set to decline throughout the 20s’ decade. It will not absorb the over investment in infrastructure, buildings, etc. The Evergrande debacle is the tip of the iceberg as Evergrande is a template for most other real estate companies in China. As the property market is highly dispersed (geographically and in assets holdings), Evergrande was relatively easy to contain by the Chinese government. The risk however, is that Evergrande is akin to the subprime debacle in the US, in 2006, which eventually led to a full-blown crisis that culminated in 2008 with Lehman Brothers’ bankruptcy. This risk is high and should not be overlooked, as we believe that in the next couple of years a full-blown crisis will unfold, possibly at its worst in 2023. If Chinese authorities let the market do its work, while maintaining systemic integrity (keep moral hazard in check), China will emerge stronger after its crisis. The crisis will mark the end of an era and the start of a new one in China.

Japan’s second demographic bust will coincide with China’s slowdown. Contagion from China will add to Japan’s problems. It will run ever higher budget deficits, financed in higher proportion by the central bank.

Korea will also start its demographic decline from 2020. It is highly exposed to China’s economy and we expect its government debt will rise rapidly in the coming years in order to attempt to manage the crisis.

The synchronised slowdown/decline of these three Asian powerhouses, together with possible contagion effects will likely result in a severe “Asian crisis”. Spillovers are unpredictable. Investors should monitor companies’ and banks’ exposure to East-Asia.

With the 2020-2021 Covid-19 pandemic, governments ran record deficits financed by the central bank. Central bank assets and monetary aggregates exploded by 50% or more in only 1 year. By late 2020, inflation made a resurgence. Economists at central banks argue that it is a temporary phenomenon driven by extraordinary measures (temporary in nature) and due to disruption in global supply chains or lower worker mobility which will normalise once the pandemic is over. These economists argue that high debt levels, debt deleveraging and demographic stagnation are powerful deflationary forces that make a scenario of deflation the main risk.

We agree that the macroeconomic backdrop of slowing demographics and debt deleveraging are powerful drivers of a deflationary environment, but we also believe that the recent expansion in central banks’ balance sheets, together with the ongoing demographic recovery in the US (echo boomers and millennials) can lead to persistent inflation in the coming decade (See chapter 8 of the book). The fact that policy makers are dovish (relaxed) regarding inflation concerns might lead to a policy mistake that leads to bursts of high inflation.

The high debt levels in the US and across the world, mean if rates rise with inflation, a crisis will likely ensue. We expect that the next major crisis, led by real estate, will occur around 2026, driven likely by rising inflation and rising rates.

The risk of higher inflation in the coming decade should not be overlooked as even if central banks and government economists convince the markets that it is under control and is temporary in nature (so that bond yields do not rise in lockstep with inflation), bond investors will lose money nonetheless as when these bonds mature the principal will have much lower purchasing power.

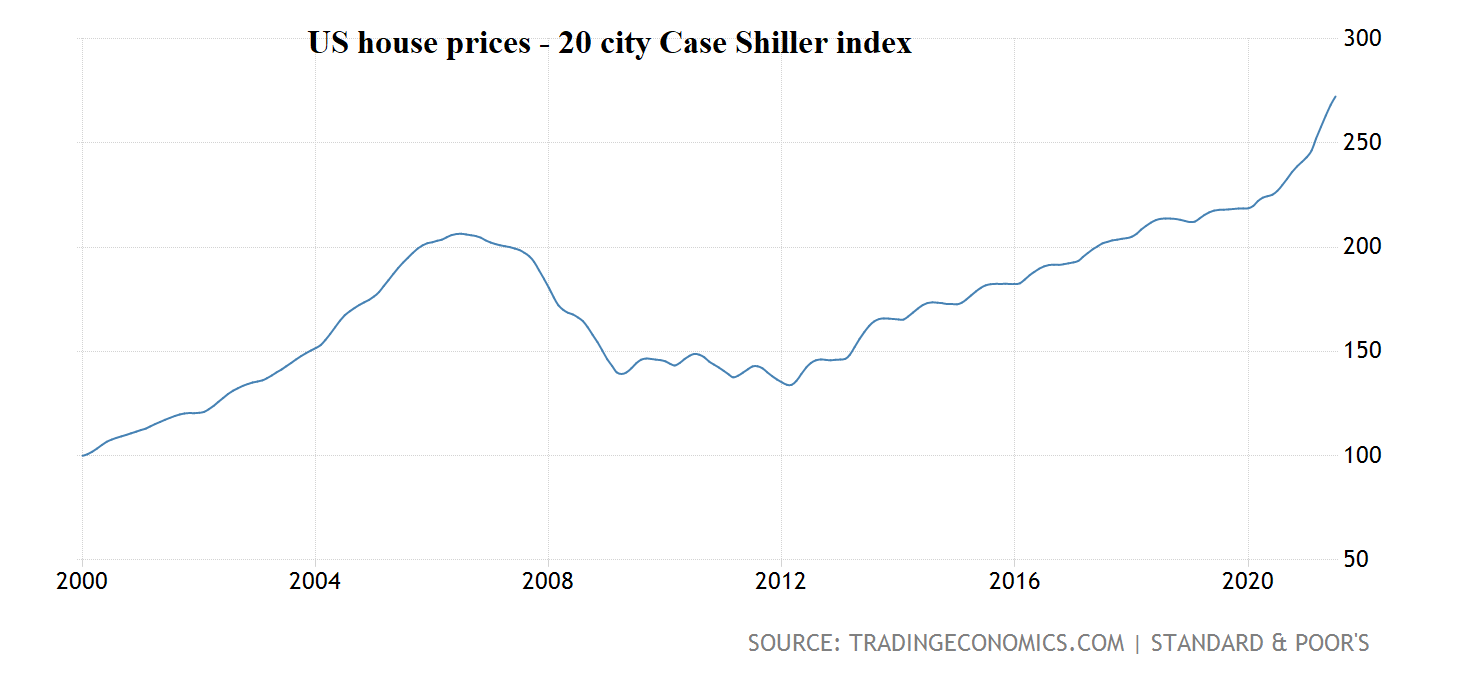

After bottoming in the aftermath of the 2008 housing crisis, US house prices rebounded, and in 2018 they surpassed their previous 2006 peak levels. Since then, particularly since 2020 (due to the extraordinary government measures during the Covid-19 pandemic), house prices soared. Quoting Robert Shiller: “The rocket took off (again)”.

The rise in house prices was driven by the millennial generation’s recent pick up in demand for owning their own house. This generation had a home-ownership rate of only about 40% in 2018 and is now up to 47.9%. This is still a lot below the “normal” home-ownership rate of 60%-65% which means that there is plenty of possible future demand. In terms of supply, the long period of low housing starts after the 2008 crisis and slow pickup thereafter means that houses are in short supply. Low supply and high demand are a recipe for rocketing prices. If you add to the fuel, ultra-low interest rates and other extraordinary measures during the pandemic, the conditions are set for a bubble to emerge.

Are house prices in a bubble? When will a crisis emerge? From what drivers?

House prices are likely at the start of a bubble which has still got room to run. Supporting the bubble are the strong demographic demand and ultra-accommodative central bank policy stance. The Fed has vowed not to raise rates until about 2024, so there is ample room for continued house price demand. In terms of housing supply, we expect house building to continue increasing up to 2025-2026. However, the pent-up demand from millennials will likely absorb the new housing inventory.

A crisis is likely to emerge when rates increase. This could be precipitated by rising inflation as the economy will be robust, supported by housing demand and real rates will be very negative. We expect that the market will be able to accommodate an initial rise in inflation and rates, but later those pressures, together with high house valuations, will take its toll and precipitate a real estate crisis around 2026.

The recent developments in Europe reduced some concerns for where the next crisis might emerge. Namely, before 2020, countries such as Portugal, Spain, Italy and the Netherlands managed to reduce debt. Therefore, the risk of a crisis emerging there is now reduced. However, some countries accumulated substantial debt since 2016 and could be trigger points for a future European “drama”.

France is such a country. It increased debt substantially from 2016 to 2020 and even more during the 2020-2021 Covid-19 pandemic as it enacted very austere measures. Its internal politics and high debt levels make it a candidate for future instability.

Greece is deeper in the hole than before. Its debt increased substantially since the European crisis as it did not follow the path of Spain and Portugal. Its debt looks clearly unsustainable and with its coming demographic decline, we expect renewed drama coming from Greece and the strong possibility of a Grexit occurring.

The timing for any European troubles is very difficult to predict as it will likely be driven by internal politics and election cycles.